Chips, oil, and gas - What’s cooking?

Part 4

Part 4

The following article was written in the week of the 19th-23rd of September 2022. Due to Substack’s publishing limitations, the article is broken down into 6 independent parts.

The events that unfolded in the week after (the 24th-30th of September 2022) made some chart and price data presented here, partially outdated.

The core narrative outlined in the article did not change.

Part 4 - A safe investment

What happens when the costs of servicing debts become higher than the total disposable income?

The risk of a debt crisis concerns not only private households but also companies and governments as well. The rate hikes affect existing corporate debt, commercial properties, investment portfolios, and can lead to widespread corporate bankruptcies, further weakening the economy. The sovereign debt levels of each of the EU states are another giant issue. Generally, investors perceive sovereign bonds to be ‘a safe investment’, lending money to governments. For example, banks and pension funds are also investors, that hold government bonds as part of their portfolios. Besides, banks and governments lend other banks or governments money. The European Union’s sovereign bond market is fragmented, with its member states having different bonds ‘quality’, or risk and yield levels. German bonds are less risky than Slovakia’s, for example.

An effect of the global financial crisis in 2008 was a sovereign debt crisis of EU member states, mainly of the southern EU countries. Do you remember how governments bailed out indebted banks? Do you remember the Greece sovereign debt crisis and how Germany bailed Greece out? Due to the very close interconnection between the banking sector and government debt, major disruptions to the real economy and the entire financial sector are inevitable. This is also known as Sovereign-Bank Diabolic Loop.

The total sovereign debt will keep rising due to the rising interest rates, thus increasing the risk of governments defaulting. In 2008 Greece partially defaulted on its government bonds (haircut), despite the bailout, and other EU member states felt the negative effects. Any investor who held Greece’s bonds in their portfolio lost money: banks, governments, investment and pension funds, private investors, etc. When pension funds go insolvent and bankrupt, many people lose their life savings and future pensions. A dire socioeconomic fallout no politician would want to deal with.

At the end of the 1st Quarter of 2022, the sovereign debt-to-GDP ratios of EU member states paint a grim picture:

Highest ratios were recorded in Greece (189.3%), Italy (152.6%), Portugal (127.0%), Spain (117.7%), and France (114.4%). A side note: Italy is the EU’s third-largest economy.

Governments owe money… and need more

Government debt has increased heavily across EU member states since Covid started. Fiscal spending was necessary to support households and companies, and to literally save the economy from total collapse. We had lockdowns and isolation. Almost the entire economy, except for certain ‘system relevant’ parts, was forcibly shut down. At present, we have another EU-wide crisis with governmental support programmes and subsidies coming in many different names, forms, and sizes. Have you ever heard of the term ‘helicopter money’? This is money that is sent directly to people’s bank accounts to support high living and energy costs. There are also ‘Climate Bonus Checks’, ‘Energy Bills Relief’, ‘Safe Housing Support’, ‘Kindergarten Vouchers’, and so on. The labels differ, but the principle is the same. Politicians love such subsidies in crisis times, especially before new elections.

This is also fiscal spending that is financed mainly by taking on new debt, whilst the budgetary deficit grows. Generally, the tax income of individual EU governments is insufficient to finance such spending and differs amongst EU member states. A weakened economy means less tax income, and insolvent companies and unemployed people pay no (or less) taxes. Simply put, it is not sustainable. The irony of using such fiscal methods is that the inflation is further exacerbated as the money supply in the economy increases. It is another feedback loop toward inflationary depression and currency collapse.

The increasing risk of a sovereign debt crisis is an elephant in the room that few officials talk about in public.

With already high inflation and announced further rate hikes by the ECB set out for this October, any monthly loan payments with variable interest rates become substantially higher. This puts private household budgets under major stress, further shrinking any disposable income, with debt defaults and private bankruptcy often being unavoidable. The same goes for indebted companies, banks, states, etc.

Between 19th and 23rd of September 2022, there was a tsunami of rate hikes by many central banks around the world in an attempt to fight soaring prices: the U.S. FED, Sweden’s Riksbank, Bank of Japan, Swiss National Bank, Bank of England, Norway’s Norges Bank, Indonesia, Taiwan, Brazil, Philippines, South Africa and a handful of others.

In an interview on the 21st of September 2022, Kristalina Georgieva, Managing Director of the International Monetary Fund, said that “Increased interest rates will bite and we will see the impact on growth “, adding that “For hundreds of millions of people it will feel like a recession, so buckle up.”

To repeat the, now rhetorical, question from before:

What happens when the costs of servicing debts become higher than the total disposable income?

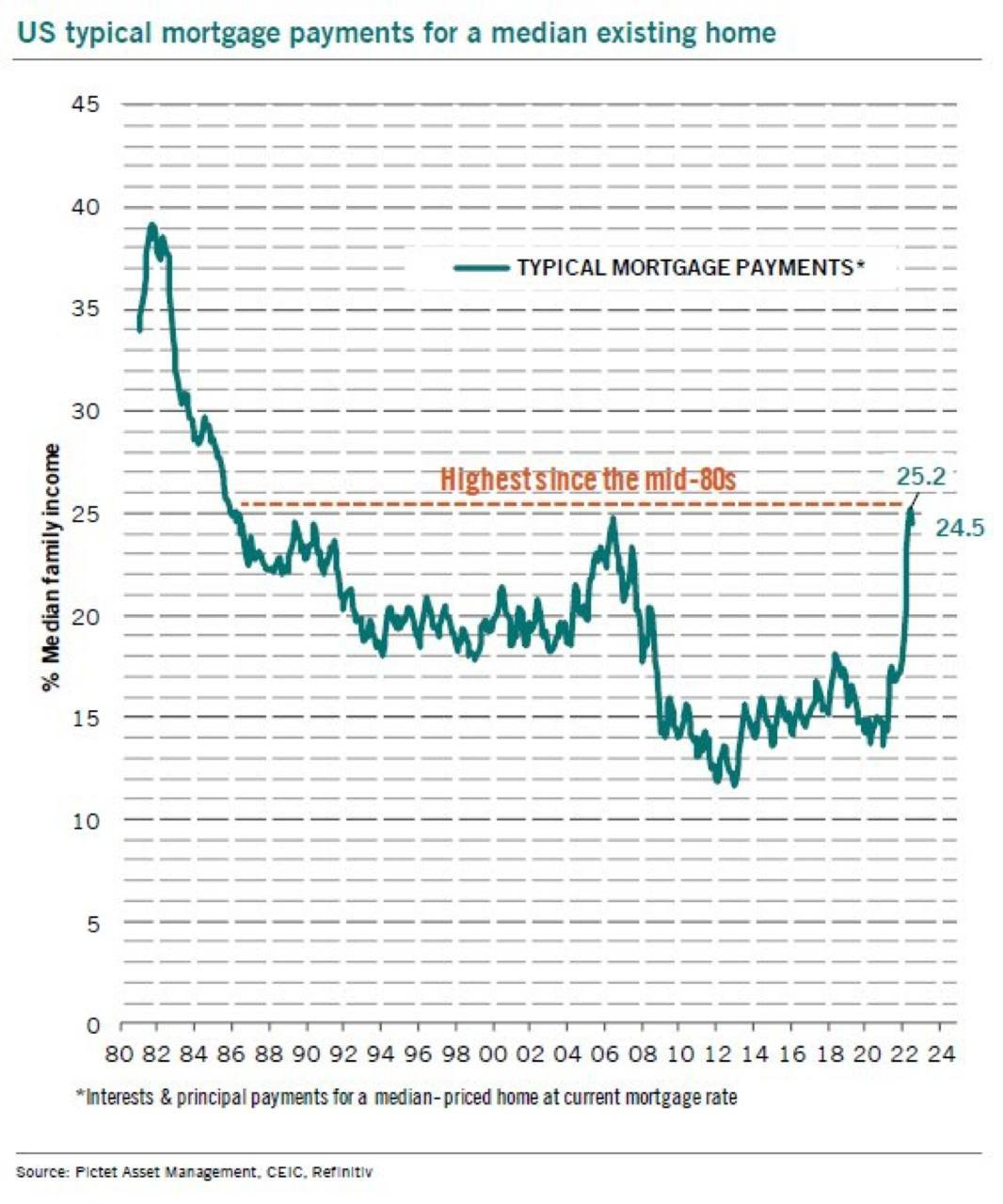

Concerning the above-mentioned EU mortgages, in the U.S., the latest data show that typical mortgage payments already make up more than 25% of the median family income. It is the highest since the mid-1980s. Less than two years ago in 2020, it was under 15%.

The rate hikes and tightening monetary policy by central banks around the globe have only started. And winter is not even here yet! Neither literally as a season nor as a figure of speech.

-- continue reading Part 5 here

Chips, oil, and gas - What’s cooking?

Part 5

The following article was written in the week of the 19th-23rd of September 2022. Due to Substack’s publishing limitations, the article is broken down into 6 independent parts. The events that unfolded in the week after (the 24th-30th of September 2022) made some chart and price data presented here, partially outdated.

or

Start over and read from the beginning: Part 1

Chips, oil, and gas - What’s cooking?

The following article was written in the week of the 19th-23rd of September 2022. Due to Substack’s publishing limitations, the article is broken down into 6 independent parts. The events that unfolded in the week after (the 24th-30th of September 2022) made some chart and price data presented here, partially outdated.