Chips, oil, and gas - What’s cooking?

Part 3

Part 3

The following article was written in the week of the 19th-23rd of September 2022. Due to Substack’s publishing limitations, the article is broken down into 6 independent parts.

The events that unfolded in the week after (the 24th-30th of September 2022) made some chart and price data presented here, partially outdated.

The core narrative outlined in the article did not change.

Part 3 - Germany is going to be all right…right?!

The outlook given by the president of the German Federal Bank (Bundesbank, a.k.a. BUND), Joachim Nagel, is sombre. He stated in September 2022 that he expects a longer recession, further rate hikes, and a two-digit inflation by year’s end.

The prices of Germany’s 10-year bonds are an indicator of the expected economic stability of the bond issuer, the Bund. It shows the willingness of investors to lend money to Germany, at different yields or rates, over time. As we can see in the below graph, the yield investors ask surged significantly in very short period of time. After one year, the costs for the Bund to lend money went from negative -0.5% to 1.8% (as of the time of writing this article). The borrowing costs are back at early 2014 levels, which is an increase of over 360%.

For bond markets, this is huge.

For the U.S. 10-year bonds investors presently ask a 3.55% yield, a year ago it was 1.25%. The yields are even higher for 2-year bonds, both for Germany and the U.S. (see addendum for charts data). The UK’s bonds are surging up as well. Higher risk countries, or economies, like emerging markets, (must) borrow at higher rates to finance their government’s expenditures. For developed economies, the risks and thus bond yield rates are usually very low. Currently high yield bonds for Germany, the U.S. and the UK mean that the borrowing and financing costs of these countries have rapidly and immensely increased.

With rate hikes to continue further, servicing existing sovereign debts and fiscal deficits, combined with decreased availability of cheap new credits paints a grim economic outlook. This fact is alarming and terrifying.

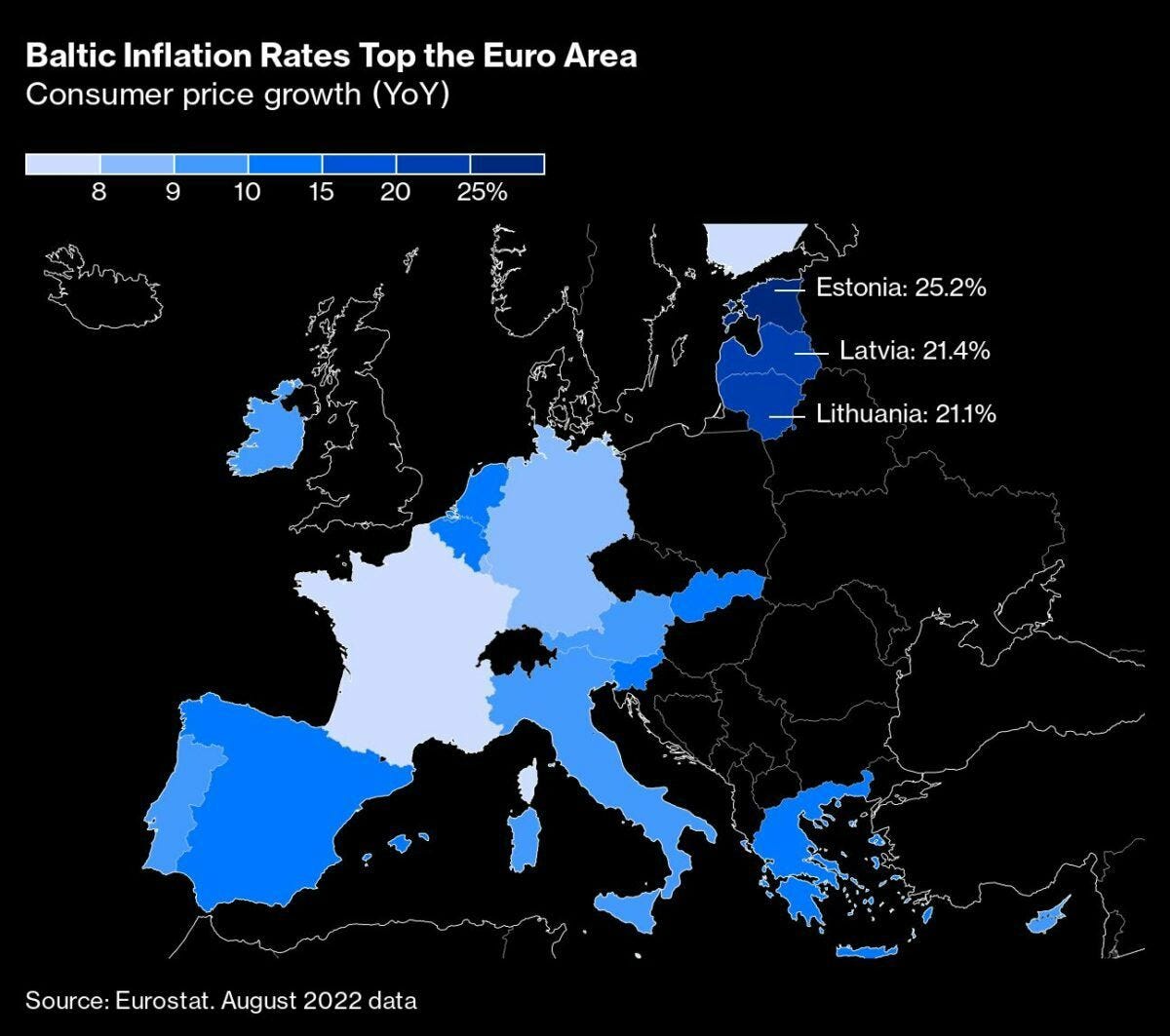

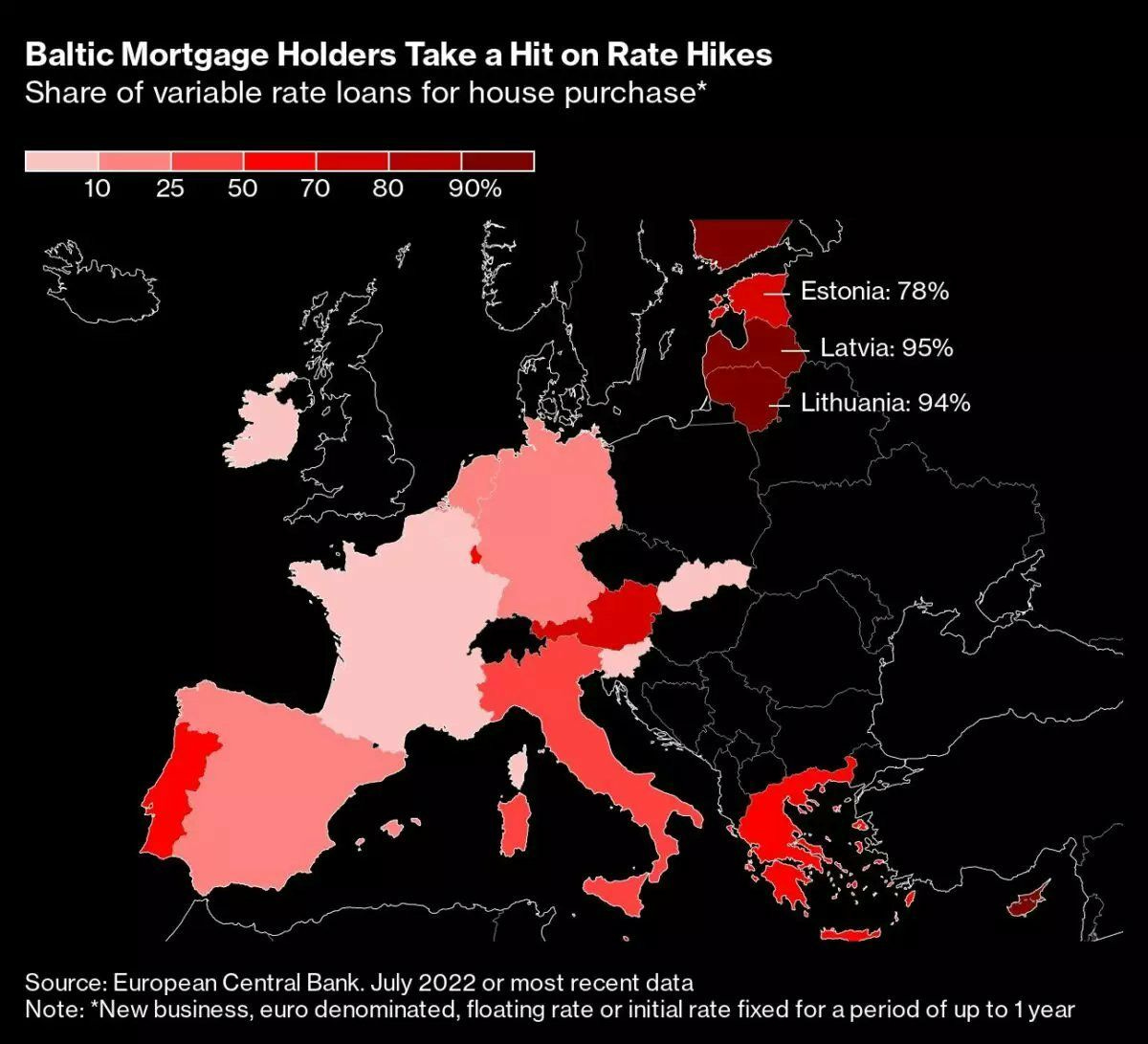

Any form of loan or debt with variable interest rates is affected by changes in a central bank’s rates. The following illustration depict the inflation and mortgages impacted by rate hikes (introduced to fight the current inflation), per EU country.

In summary: The illustrations show an increased risk and a high probability of EU-wide mortgage defaults.

What would happen if this were the case?

A likely scenario:

Many people suddenly can’t afford home loan repayments; banks take ownership and sell properties (foreclosure process). New buyers or loan takers are nowhere to be found since people are in ‘survival mode’, and banks are reluctant to grant new credit, prioritising their own solvency preservation. Banks seeking to remove depreciating assets off their balance sheets will start market-selling foreclosed properties. This results in crashing real-estate prices, forcing (other) banks to sell at (even lower) market prices. There are too few homebuyers and too many properties offered for sale, causing lower bids. From a seller’s perspective: I need to sell immediately! From a buyer’s perspective: Why buy cheap now if I can buy even cheaper tomorrow? It is a negative feedback loop. One can easily draw parallels here to the Great Financial Crisis of 2008, with the bursting of the U.S. housing bubble…

It appears that, presently, one of the most underestimated or overlooked risks for Europe are sharply rising interest rates, which would trigger a debt crisis.

On the 21st of September 2022, the Vice President of the European Central Bank (ECB), Luis De Guindos said: “[rate] hikes to continue and data will determine the size”. Isabell Schnabel, a board member of the ECB, said on the 22nd of Sept.-22 that the current inflation is too high, and that the Eurozone is facing an economic downturn. She concludes that “we [the ECB] need to continue raising rates”, and adds that a recession in Germany may be unavoidable due to its gas dependence.

The ECB’s De Guindos and Schnabel statements are in line with Bundesbank’s president Nagel statements, mentioned earlier in this article. These were public statements just a few days apart, confirming that there is a consensus amongst the highest decision makers in the EU’s banking circles.

A nota bene:

The ECB is part of the Eurosystem, which is the monetary authority of the Eurozone, and its primary purpose is to maintain the price stability.

What happens when the costs of servicing debts become higher than the total disposable income?

-- continue reading Part 4 here

Chips, oil, and gas - What’s cooking?

Part 4

The following article was written in the week of the 19th-23rd of September 2022. Due to Substack’s publishing limitations, the article is broken down into 6 independent parts. The events that unfolded in the week after (the 24th-30th of September 2022) made some chart and price data presented here, partially outdated.

or

Start over and read from the beginning: Part 1

Chips, oil, and gas - What’s cooking?

The following article was written in the week of the 19th-23rd of September 2022. Due to Substack’s publishing limitations, the article is broken down into 6 independent parts. The events that unfolded in the week after (the 24th-30th of September 2022) made some chart and price data presented here, partially outdated.